Motivation

Methodology

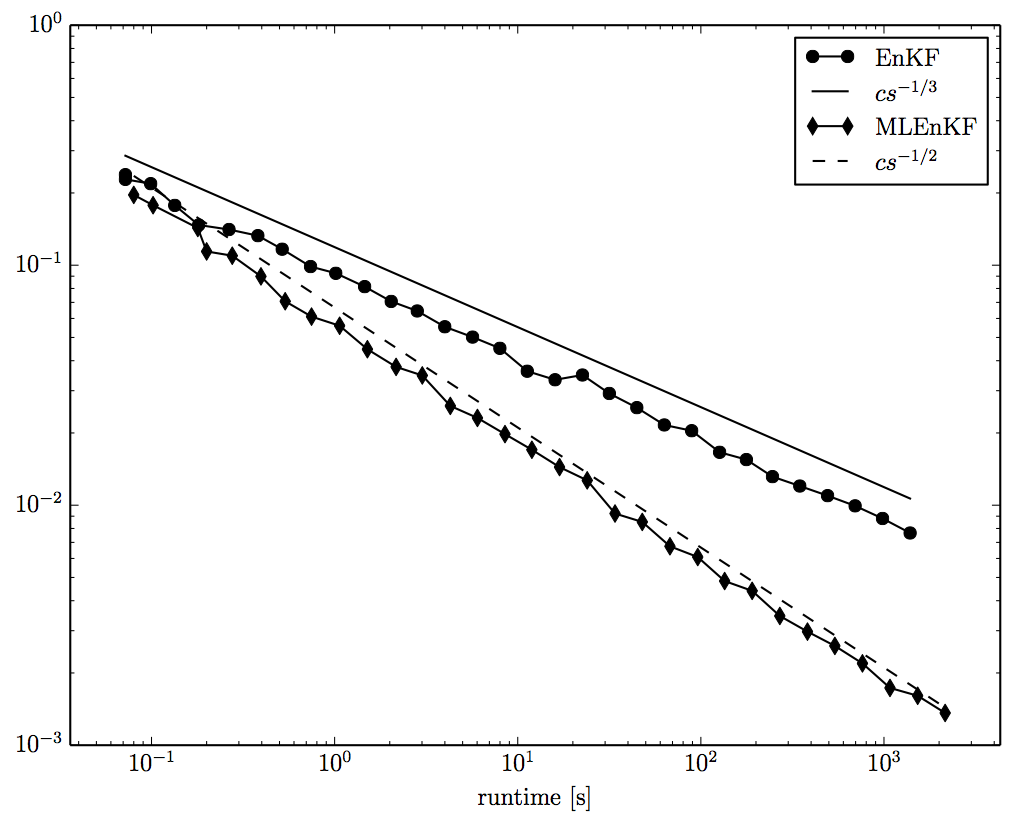

For problems which admit hierarchies of approximations with cost inversely proportional to accuracy, it is natural to leverage solutions to less expensive and less accurate approximations in order to accelerate the convergence of the more expensive and more accurate approximations. The multilevel Monte Carlo (MLMC) is an extension of classical Monte Carlo methods which by sampling stochastic realizations on a hierarchy of resolutions may reduce the computational cost of moment approximations by orders of magnitude. In this project we have combined the ideas of MLMC and EnKF to give rise to the multilevel Ensemble Kalman Filtering method (MLEnKF). MLEnKF is constructed to compute particle paths on a hierarchy of accuracy levels, in this case given by increasing refinement of the temporal discretization, and the Kalman Filter update formulas are extended to multilevel update formulas for means and covariances on the full ensemble hierarchy of particle simulations [1]

Outcome

Theoretical proofs and numerical studies showing that MLEnKF asymptotically approximates filtering distributions orders of magnitude more efficiently than EnKF [1].

Figure 1: The error decay for EnKF and MLEnKF as a function of the computational runtime for filtering problem whose underlying dynamics is a Ornstein-Uhlenbeck process. The error is measured in root mean square errors (RMSE) between the exact Kalman filter mean and covariance moments and the corresponding moments from EnKF and MLEnK.

Multilevel ensemble Kalman filtering, arXiv preprint arXiv:1502.06069, 2015.

Multilevel ensemble Kalman filtering, arXiv preprint arXiv:1502.06069, 2015.